Property taxation: exemptions: Chiquita Canyon elevated temperature landfill event.

Exempts properties affected by the Chiquita Canyon landfill event from property taxes through 2030. Takes effect immediately upon passage and expires on January 1, 2031. Requires counties to implement the tax exemption without state reimbursement for lost revenue.

Property taxation: exemptions: Chiquita Canyon elevated temperature landfill event.

Exempts properties affected by the Chiquita Canyon landfill event from property taxes through 2030. Takes effect immediately upon passage and expires on January 1, 2031. Requires counties to implement the tax exemption without state reimbursement for lost revenue.

Taxation: information returns: vacant commercial real property.

Requires commercial property owners to file annual reports on vacant buildings starting in 2025. Imposes a $100 penalty per property for failing to submit required vacancy information. Mandates the state tax department to publish annual vacancy data by ZIP code. Establishes a temporary program that automatically expires on January 1, 2031.

Taxation: information returns: vacant commercial real property.

Requires commercial property owners to file annual reports on vacant buildings starting in 2025. Imposes a $100 penalty per property for failing to submit required vacancy information. Mandates the state tax department to publish annual vacancy data by ZIP code. Establishes a temporary program that automatically expires on January 1, 2031.

Personal income taxes: unemployment insurance: tips.

Excludes tips from California personal income tax and unemployment insurance calculations from 2026 through 2030. Requires employees to report tips to employers monthly through written statements by the 10th of each month. Modifies employer payroll withholding requirements to exclude tips from wage calculations. Mandates the Franchise Tax Board to report on tax returns claiming the tip exemption by December 2036.

Personal income taxes: unemployment insurance: tips.

Excludes tips from California personal income tax and unemployment insurance calculations from 2026 through 2030. Requires employees to report tips to employers monthly through written statements by the 10th of each month. Modifies employer payroll withholding requirements to exclude tips from wage calculations. Mandates the Franchise Tax Board to report on tax returns claiming the tip exemption by December 2036.

Personal income taxes: credit: medical services: rural areas.

Establishes a $5,000 annual tax credit for medical professionals who provide services in rural California areas. Applies to licensed healthcare providers including doctors, nurses, dentists, and therapists from 2026 through 2030. Excludes telehealth services and cosmetic procedures from qualifying for the tax credit. Requires the Franchise Tax Board to report on program effectiveness by January 2030.

Personal income taxes: credit: medical services: rural areas.

Establishes a $5,000 annual tax credit for medical professionals who provide services in rural California areas. Applies to licensed healthcare providers including doctors, nurses, dentists, and therapists from 2026 through 2030. Excludes telehealth services and cosmetic procedures from qualifying for the tax credit. Requires the Franchise Tax Board to report on program effectiveness by January 2030.

Personal Income Tax Law: credits: insurance.

Establishes a new tax credit for California homeowners to offset rising residential property insurance costs. Provides credits for insurance premium increases above 2023 baseline costs through 2031. Limits eligibility to primary residences purchased before 2024 and households earning under $300,000 annually. Requires annual reporting starting July 2028 to track the program's effectiveness in controlling premium costs.

Personal Income Tax Law: credits: insurance.

Establishes a new tax credit for California homeowners to offset rising residential property insurance costs. Provides credits for insurance premium increases above 2023 baseline costs through 2031. Limits eligibility to primary residences purchased before 2024 and households earning under $300,000 annually. Requires annual reporting starting July 2028 to track the program's effectiveness in controlling premium costs.

Public social services: tax-exempt nonprofit organizations.

Updates eligibility rules to treat state tax-exempt status as qualifying for grants. Establishes ESAVN to provide resettlement services for asylees and vulnerable noncitizens. Requires grant recipients to have three years' experience and malpractice insurance. Enacts as an urgency statute with immediate effect.

Public social services: tax-exempt nonprofit organizations.

Updates eligibility rules to treat state tax-exempt status as qualifying for grants. Establishes ESAVN to provide resettlement services for asylees and vulnerable noncitizens. Requires grant recipients to have three years' experience and malpractice insurance. Enacts as an urgency statute with immediate effect.

Personal Income Tax Law: credits: medical expenses.

Establishes a new state tax deduction of up to $5,000 for out-of-pocket medical expenses. Takes effect January 2025 and automatically expires in December 2030. Requires annual reports tracking the number of taxpayers claiming the deduction and average amounts. Applies only to medical costs not covered by insurance or other reimbursements.

Personal Income Tax Law: credits: medical expenses.

Establishes a new state tax deduction of up to $5,000 for out-of-pocket medical expenses. Takes effect January 2025 and automatically expires in December 2030. Requires annual reports tracking the number of taxpayers claiming the deduction and average amounts. Applies only to medical costs not covered by insurance or other reimbursements.

Personal income tax: rate.

Reduces California personal income tax rates by 1-2 percentage points across all brackets from 2025 through 2029. Increases income thresholds for tax brackets to allow higher earnings before higher rates apply. Implements annual inflation adjustments to tax brackets starting in 2026 based on California Consumer Price Index. Takes effect immediately as a tax levy with changes applying to income earned starting January 1, 2025.

Personal income tax: rate.

Reduces California personal income tax rates by 1-2 percentage points across all brackets from 2025 through 2029. Increases income thresholds for tax brackets to allow higher earnings before higher rates apply. Implements annual inflation adjustments to tax brackets starting in 2026 based on California Consumer Price Index. Takes effect immediately as a tax levy with changes applying to income earned starting January 1, 2025.

Personal income tax: credit: home security surveillance.

Provides California homeowners with a $250 tax credit for installing security surveillance systems from 2026 to 2031. Covers 100% of purchase and installation costs for video, audio, or photographic security devices up to the credit limit. Allows unused portions of the credit to be carried forward for up to eight years. Requires annual reporting from the Franchise Tax Board on the number of taxpayers claiming the credit.

Personal income tax: credit: home security surveillance.

Provides California homeowners with a $250 tax credit for installing security surveillance systems from 2026 to 2031. Covers 100% of purchase and installation costs for video, audio, or photographic security devices up to the credit limit. Allows unused portions of the credit to be carried forward for up to eight years. Requires annual reporting from the Franchise Tax Board on the number of taxpayers claiming the credit.

Personal Income Tax Law: Corporation Tax Law: credits: retail security measures.

Establishes a new tax credit of up to $10,000 for retail businesses to invest in theft prevention measures. Covers security equipment including cameras, alarms, lighting, and license plate readers. Applies to retail businesses from 2025 through 2029 with different thresholds based on employee count. Requires the Franchise Tax Board to report annually on credit usage starting April 2028.

Personal Income Tax Law: Corporation Tax Law: credits: retail security measures.

Establishes a new tax credit of up to $10,000 for retail businesses to invest in theft prevention measures. Covers security equipment including cameras, alarms, lighting, and license plate readers. Applies to retail businesses from 2025 through 2029 with different thresholds based on employee count. Requires the Franchise Tax Board to report annually on credit usage starting April 2028.

Employment: employer contributions: employee withholdings: credit: agricultural employees.

Establishes a new tax credit for agricultural employers who pay overtime wages to farmworkers. Allows employers to claim credits equal to overtime wages paid, up to their quarterly withholding amount. Maintains existing tax withholding requirements for both employers and employees. Authorizes the Employment Development Department to create rules for implementing the credit system.

Employment: employer contributions: employee withholdings: credit: agricultural employees.

Establishes a new tax credit for agricultural employers who pay overtime wages to farmworkers. Allows employers to claim credits equal to overtime wages paid, up to their quarterly withholding amount. Maintains existing tax withholding requirements for both employers and employees. Authorizes the Employment Development Department to create rules for implementing the credit system.

Personal income taxes: credit: manufacturing: sales and use taxes.

Establishes new tax credits for manufacturers and researchers to offset local sales taxes from 2026 through 2030. Requires annual revenue impact reports to legislative budget committees starting May 2026. Allows unused credits to be carried forward for up to eight years if they exceed the tax liability. Mandates businesses to file amended returns if qualifying equipment moves out of state within one year.

Personal income taxes: credit: manufacturing: sales and use taxes.

Establishes new tax credits for manufacturers and researchers to offset local sales taxes from 2026 through 2030. Requires annual revenue impact reports to legislative budget committees starting May 2026. Allows unused credits to be carried forward for up to eight years if they exceed the tax liability. Mandates businesses to file amended returns if qualifying equipment moves out of state within one year.

Personal Income Tax Law: exclusions: first responders: overtime pay.

Exempts overtime pay from state income tax for first responders working during declared disasters. Applies to emergency response work performed between 2025 and 2030 in disaster-declared counties. Covers first responders who live or work in affected counties or are deployed through mutual aid. Authorizes the Franchise Tax Board to establish verification procedures and documentation requirements.

Personal Income Tax Law: exclusions: first responders: overtime pay.

Exempts overtime pay from state income tax for first responders working during declared disasters. Applies to emergency response work performed between 2025 and 2030 in disaster-declared counties. Covers first responders who live or work in affected counties or are deployed through mutual aid. Authorizes the Franchise Tax Board to establish verification procedures and documentation requirements.

Personal Income Tax Law: exclusions: first responders: overtime pay.

Exempts overtime wages earned by first responders during declared emergencies from state income tax through 2029. Applies to emergency medical technicians, paramedics, ambulance drivers, and other first responders. Takes effect immediately and automatically expires on December 1, 2030. Authorizes the Franchise Tax Board to establish verification procedures and documentation requirements.

Personal Income Tax Law: exclusions: first responders: overtime pay.

Exempts overtime wages earned by first responders during declared emergencies from state income tax through 2029. Applies to emergency medical technicians, paramedics, ambulance drivers, and other first responders. Takes effect immediately and automatically expires on December 1, 2030. Authorizes the Franchise Tax Board to establish verification procedures and documentation requirements.

Personal Income Tax Law: exclusions: first responders.

Exempts wages from state income tax for local first responders who assist during emergencies outside their jurisdiction. Creates a five-year tax benefit program running from January 2025 through December 2030. Applies only to emergency response work performed outside a first responder's regular service area. Authorizes the Franchise Tax Board to establish verification procedures and documentation requirements.

Personal Income Tax Law: exclusions: first responders.

Exempts wages from state income tax for local first responders who assist during emergencies outside their jurisdiction. Creates a five-year tax benefit program running from January 2025 through December 2030. Applies only to emergency response work performed outside a first responder's regular service area. Authorizes the Franchise Tax Board to establish verification procedures and documentation requirements.

Taxation: renter’s credit.

Increases the California renter's tax credit from $120 to $2,000 for joint filers and from $60 to $1,000 for individuals. Expands income eligibility limits to $150,000 for joint filers and $75,000 for individuals. Makes the expanded credit refundable, allowing renters to receive the full amount even if it exceeds their tax liability. Requires annual inflation adjustments to credit amounts and income limits for five years once funded.

Taxation: renter’s credit.

Increases the California renter's tax credit from $120 to $2,000 for joint filers and from $60 to $1,000 for individuals. Expands income eligibility limits to $150,000 for joint filers and $75,000 for individuals. Makes the expanded credit refundable, allowing renters to receive the full amount even if it exceeds their tax liability. Requires annual inflation adjustments to credit amounts and income limits for five years once funded.

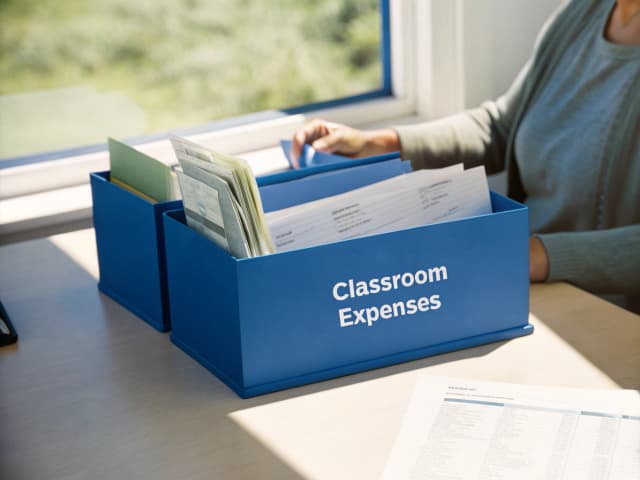

Personal Income Tax Law: deduction: teachers.

Allows California teachers to deduct classroom supplies and professional development expenses from state taxes. Aligns state tax law with federal deductions for teachers from 2026 through 2030. Requires the Franchise Tax Board to track deduction claims and evaluate their benefit to students. Takes effect immediately to support teachers who pay out-of-pocket for classroom materials.

Personal Income Tax Law: deduction: teachers.

Allows California teachers to deduct classroom supplies and professional development expenses from state taxes. Aligns state tax law with federal deductions for teachers from 2026 through 2030. Requires the Franchise Tax Board to track deduction claims and evaluate their benefit to students. Takes effect immediately to support teachers who pay out-of-pocket for classroom materials.

Electric vehicle charging stations: exempt entities: building standards.

Exempts churches and nonprofits from mandatory electric vehicle charging station installation requirements. Protects tax-exempt status of churches and nonprofits that install EV charging stations. Requires a report by 2030 on the number of exempt organizations installing charging stations. Maintains property tax exemptions for religious and nonprofit properties with charging stations.

Electric vehicle charging stations: exempt entities: building standards.

Exempts churches and nonprofits from mandatory electric vehicle charging station installation requirements. Protects tax-exempt status of churches and nonprofits that install EV charging stations. Requires a report by 2030 on the number of exempt organizations installing charging stations. Maintains property tax exemptions for religious and nonprofit properties with charging stations.

Income tax: exclusion: disasters.

Exempts up to $300,000 in annual income for taxpayers whose property was damaged or deemed uninhabitable by disasters. Applies to income earned during the disaster year and the following year, effective from 2025 through 2035. Covers homeowners, residents, and business owners affected by qualifying disasters. Requires affected taxpayers to provide documentation to the Franchise Tax Board upon request.

Income tax: exclusion: disasters.

Exempts up to $300,000 in annual income for taxpayers whose property was damaged or deemed uninhabitable by disasters. Applies to income earned during the disaster year and the following year, effective from 2025 through 2035. Covers homeowners, residents, and business owners affected by qualifying disasters. Requires affected taxpayers to provide documentation to the Franchise Tax Board upon request.

California Pediatric Cancer Research Voluntary Tax Contribution Fund.

Establishes a voluntary tax contribution fund for pediatric cancer research on California tax returns. Requires a minimum of $250,000 in annual contributions to maintain the program. Allocates funds to University of California for research grants and community education programs. Expires after seven years unless renewed by the Legislature.

California Pediatric Cancer Research Voluntary Tax Contribution Fund.

Establishes a voluntary tax contribution fund for pediatric cancer research on California tax returns. Requires a minimum of $250,000 in annual contributions to maintain the program. Allocates funds to University of California for research grants and community education programs. Expires after seven years unless renewed by the Legislature.

Personal income tax: exclusions: interest income: theft.

Excludes stolen or unauthorized transferred investment interest income from state taxes starting in 2026. Prevents taxpayers from claiming both the exclusion and a deduction for the same stolen interest income. Takes effect immediately as a tax levy under California law.

Personal income tax: exclusions: interest income: theft.

Excludes stolen or unauthorized transferred investment interest income from state taxes starting in 2026. Prevents taxpayers from claiming both the exclusion and a deduction for the same stolen interest income. Takes effect immediately as a tax levy under California law.

Incomplete gift nongrantor trusts: Personal Income Tax Law.

Excludes charitable remainder trusts from incomplete gift nongrantor trust status. Clarifies the exclusion is declaratory of existing law. Maintains grantor-level taxation for incomplete gift trusts unless exempt. Franchise Tax Board may issue rules to implement the change.

Incomplete gift nongrantor trusts: Personal Income Tax Law.

Excludes charitable remainder trusts from incomplete gift nongrantor trust status. Clarifies the exclusion is declaratory of existing law. Maintains grantor-level taxation for incomplete gift trusts unless exempt. Franchise Tax Board may issue rules to implement the change.

Housing: Building Home Ownership for All Program.

Establishes a new state program to make home ownership more affordable for lower and moderate-income Californians. Creates tax credits covering 40% of construction costs for builders who develop affordable for-sale housing. Targets assistance to historically excluded groups including victims of redlining and natural disasters. Requires annual program effectiveness reviews starting January 2028 through December 2031.

Housing: Building Home Ownership for All Program.

Establishes a new state program to make home ownership more affordable for lower and moderate-income Californians. Creates tax credits covering 40% of construction costs for builders who develop affordable for-sale housing. Targets assistance to historically excluded groups including victims of redlining and natural disasters. Requires annual program effectiveness reviews starting January 2028 through December 2031.

Income tax: credits: food banks.

Extends the tax credit for food donations to California food banks through January 1, 2032. Provides a 15% tax credit to farmers and processors who donate eligible food items to food banks. Requires food banks to certify donations with detailed documentation for tax credit claims. Mandates annual reporting on credit usage and donation impacts through December 2035.

Income tax: credits: food banks.

Extends the tax credit for food donations to California food banks through January 1, 2032. Provides a 15% tax credit to farmers and processors who donate eligible food items to food banks. Requires food banks to certify donations with detailed documentation for tax credit claims. Mandates annual reporting on credit usage and donation impacts through December 2035.

Annual tax: partnerships and LLCs.

Reduces the annual minimum tax for partnerships and LLCs from $800 to $80 from 2025 through 2029. Exempts small businesses owned by deployed military members from paying the annual tax under certain conditions. Requires the Franchise Tax Board to report annually on the number of affected businesses starting December 2026.

Annual tax: partnerships and LLCs.

Reduces the annual minimum tax for partnerships and LLCs from $800 to $80 from 2025 through 2029. Exempts small businesses owned by deployed military members from paying the annual tax under certain conditions. Requires the Franchise Tax Board to report annually on the number of affected businesses starting December 2026.